Why should local communities aim to introduce a lodging tax?

In recent years, discussions regarding the introduction of a lodging tax have been taking place across the country as a means of securing funding for tourism promotion. In this article, we will examine the case of Fukuoka City, where such a tax has already been implemented, to explain the basic principles behind the lodging tax and the rationale for its introduction.

1. Tourism Policy Enters a New Phase in the Post-COVID Era

On March 31, 2023, the government approved the Basic Plan for Promoting a Tourism-Oriented Nation through a Cabinet decision, outlining a new vision for a post-COVID tourism-oriented nation. This plan, the first revision in six years, aims for the sustainable revival of the tourism-oriented nation. It emphasizes improving “quality” over “quantity” and sets indicators that do not rely on visitor numbers, signaling that tourism policy has entered a new phase.Regarding inbound tourism policy, the plan sets targets for early achievement, such as 5 trillion yen in inbound spending (compared to 4.8 trillion yen in 2019) and 200,000 yen in per-person travel spending (compared to 159,000 yen in 2019). However, the plan sets 2025—the year the Osaka-Kansai World Expo is held—as the target year for the number of foreign visitors to Japan and total spending to exceed 2019 levels.

Since the classification of COVID-19 under the Infectious Diseases Control Law was downgraded to Category 5 in May 2023, activity in the service industry has been returning to normal. The number of international visitors to Japan in 2023 reached 25.07 million, recovering to approximately 80% of pre-pandemic levels, with eight countries and regions (excluding China) recording their highest annual figures, marking a V-shaped recovery from the pandemic.Furthermore, travel spending by international visitors to Japan increased by 9.9% compared to 2019, reaching 5.2923 trillion yen, and per-person travel spending amounted to 212,000 yen, achieving the target set for 2025 as early as 2023.Although the number of visitors was lower than in 2019, this can be considered an ideal outcome, with spending on travel increasing. Looking at the breakdown of per-person spending, a notable feature is that accommodation costs rose by 5.2% compared to 2019, suggesting that efforts to raise average room rates—a long-standing challenge—are bearing fruit.

On the other hand, overtourism has once again become an issue in Kyoto and Kamakura. In Kyushu, there has been a sharp increase in foreign day-trippers—primarily from South Korea—visiting Yufuin Onsen, highlighting issues such as a shortage of restrooms and litter problems. Consequently, measures to create sustainable tourism regions are urgently needed.

2. Funding Challenges for Tourism Promotion

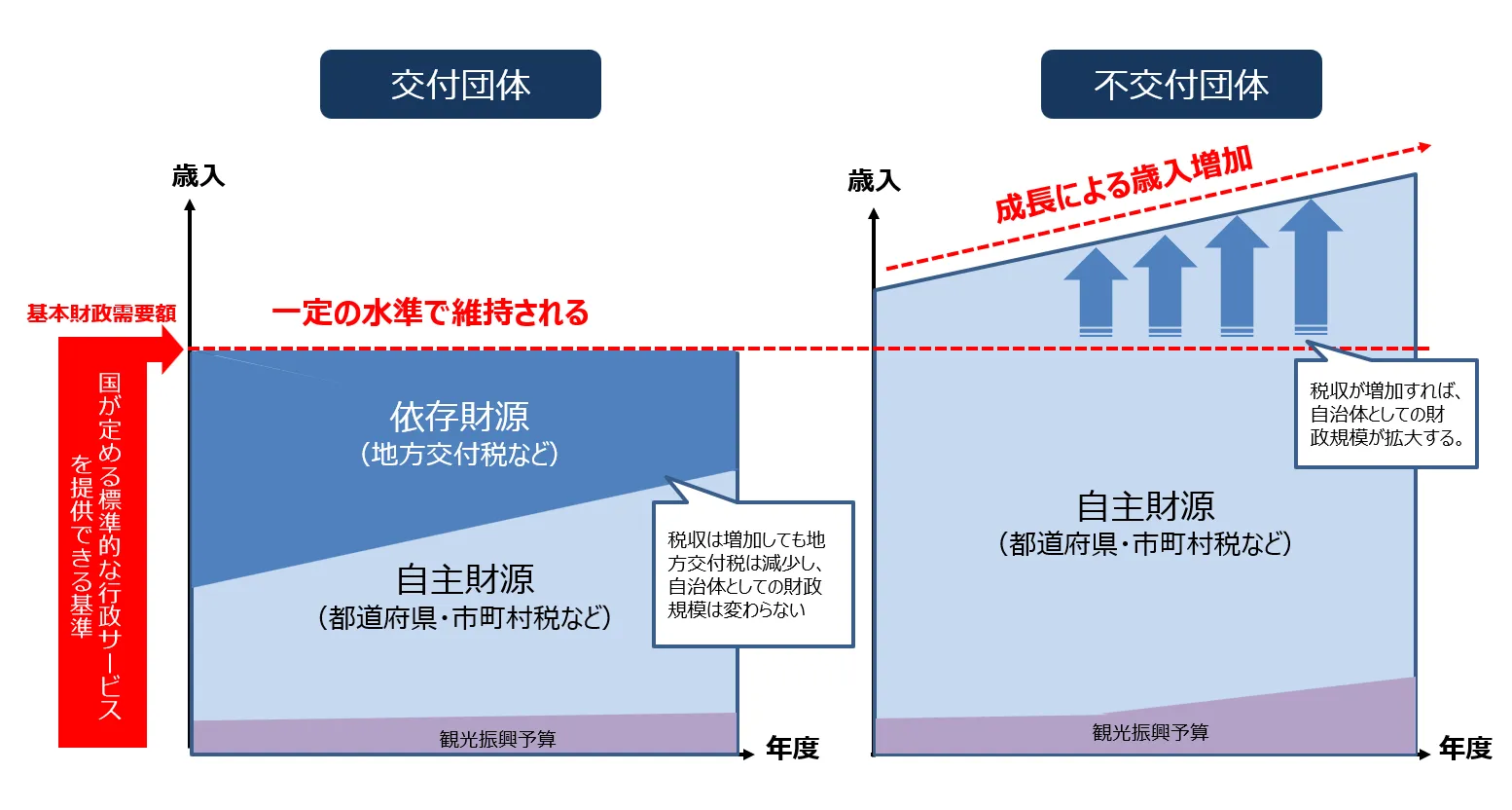

The V-shaped recovery in the number of foreign tourists and their spending has boosted momentum for strengthening tourism promotion efforts in regional cities, but a major challenge here is funding. While there are approximately 1,800 local governments nationwide, the vast majority are municipalities with weak financial capacity.The shortage of local government funds has expanded rapidly since FY 1994 due to declining tax revenues and tax cuts. Even in FY 2023, an overall funding shortfall of 2.0 trillion yen is projected, driven by factors such as the natural increase in social security-related expenses associated with an aging population. The reality is that most local governments cannot cover their expenses solely with their own revenue from local taxes and are maintained at a certain level through local allocation taxes provided by the national government.Since the independent revenue of many municipalities accounts for only about 30% to 40% of their total revenue, the majority of their income comes from dependent revenue sources such as the Local Allocation Tax.

The main sources of local governments’ independent revenue are resident taxes and property taxes. As the resident population grows, homes and buildings are constructed, and land values rise, local governments’ independent revenue increases. However, the reality is that even when independent revenue increases, the total fiscal resources of local governments do not necessarily grow.Even if a municipality succeeds in increasing its resident population or attracting businesses through its own efforts, thereby increasing its independent revenue, the system is designed such that the amount of Local Allocation Tax received from the national government is reduced. This is because the municipality’s fiscal scale is maintained at a certain level based on the “Standard Fiscal Needs Amount,” which serves as the calculation standard for Local Allocation Tax. Incidentally, this Standard Fiscal Needs Amount is intended to guarantee the financial resources necessary for municipalities to provide a certain level of administrative services to all citizens living in the region.

There is no doubt that tourism promotion is a crucial measure for revitalizing the local economy. However, the reality for local governments is that it is difficult to increase tourism budgets while grappling with various fiscal challenges. While an increase in tourists leads to higher spending by travelers, which in turn creates local jobs and ultimately contributes to an increase in the resident population, tourism promotion—such as attracting hotels and tourist facilities—can also lead to attracting businesses. This, in turn, increases independent revenue sources such as resident taxes and property taxes.However, this would result in a corresponding reduction in local allocation tax, meaning that, in the end, the local government’s finances would not actually improve. Against this backdrop, for local governments facing a shortage of financial resources, the funds available for tourism promotion are limited, and the reality is that it is difficult to significantly increase the tourism promotion budget.

Therefore, a measure attracting attention as a way to improve the financial strength of local governments is the “non-statutory new tax,” which was newly established by the amendment to the Local Tax Act in April 2000. Since this is not included in the calculation of the “standard fiscal needs amount” mentioned earlier, it contributes purely to an increase in the municipality’s revenue sources. There are two types: “non-statutory general taxes,” for which no specific use is designated, and “non-statutory purpose-specific taxes,” for which the use is specified in advance.The accommodation tax, which has been the subject of lively debate recently, is a non-statutory purpose tax that is used directly for the promotion of tourism, thereby directly increasing the budget for tourism promotion.There are various types of non-statutory new taxes. Notable examples include the “History and Culture Environmental Tax” (a non-statutory general tax) levied on parking fees in Dazaifu City, Fukuoka Prefecture, to address traffic congestion, and the “Norikura Environmental Conservation Tax” (a non-statutory purpose-specific tax) levied on parking fees at the Norikura Tsurugaike Parking Lot in Gifu Prefecture to preserve the natural environment of the Norikura region.While the lodging tax is not the only means of securing tourism budgets, the introduction of new non-statutory taxes must adhere to the “three principles of taxation”: “fairness,” “neutrality,” and “simplicity.” Regarding the lodging tax, it can be considered a simple and highly neutral tax because it allows for a fair distribution of the burden among guests and imposes a fixed charge based on the room rate.

3. Basic Concept of the Lodging Tax

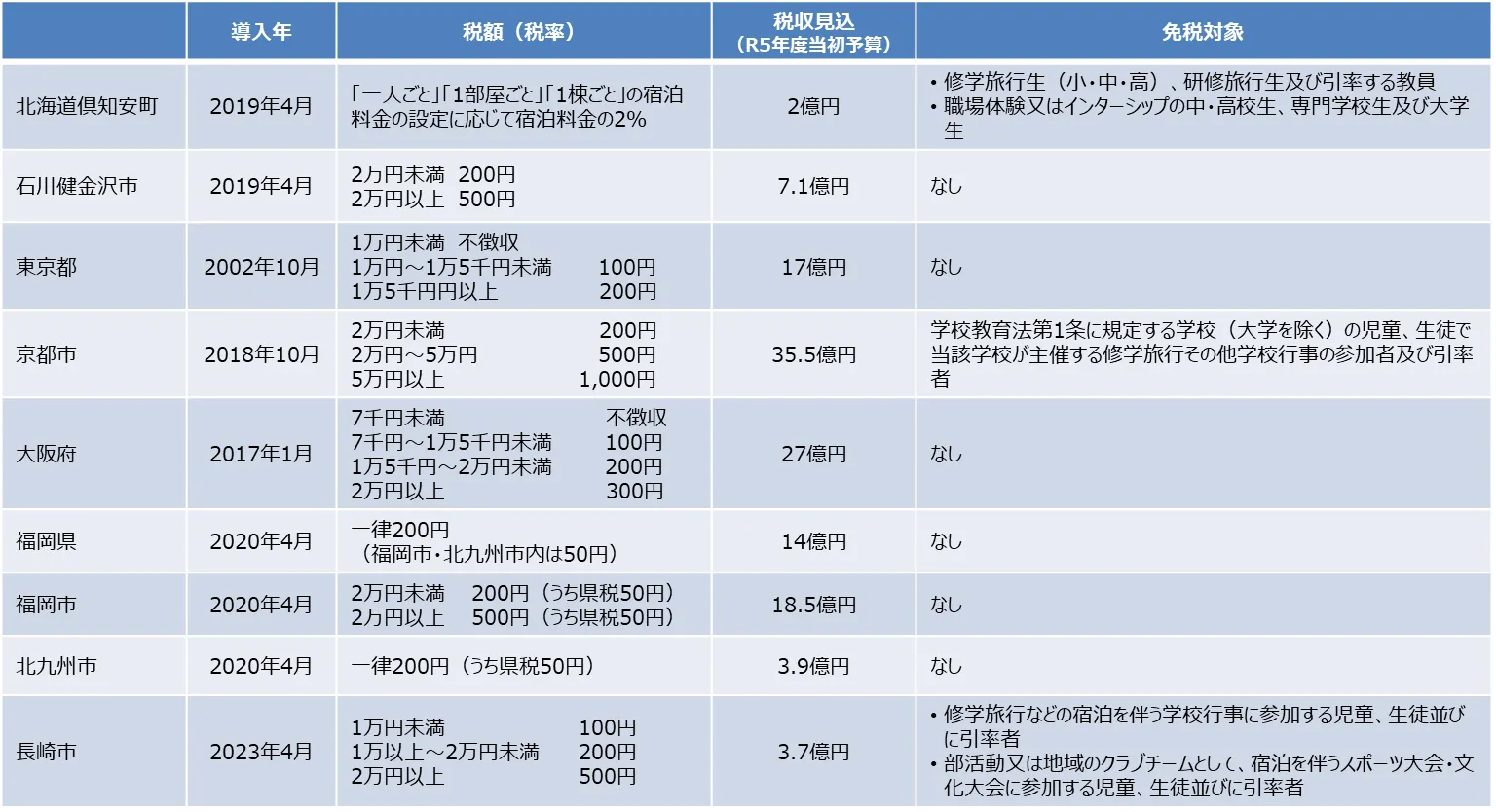

Tokyo was the first to introduce an accommodation tax following the amendment of the Local Tax Act, enacting its Accommodation Tax Ordinance in 2002. Although discussions on introducing the tax stalled for some time afterward, after Osaka Prefecture implemented it in 2017—15 years after Tokyo’s introduction—eight local governments had successfully introduced the tax by 2020 to secure funding for attracting more international visitors to Japan and promoting MICE (Meetings, Incentives, Conferences, and Exhibitions).On the other hand, some local governments have opted to raise the hot spring tax rather than introduce a lodging tax. While hot spring resorts have traditionally collected hot spring taxes, there is debate regarding the use of those funds, and as a result, many regions remain reluctant to introduce a lodging tax.

As the COVID-19 pandemic subsided in 2023 and the number of domestic and international tourists increased, movements toward introducing a lodging tax have intensified across prefectures and municipalities nationwide, with review committees being established. Most recently, Tokoname City in Aichi Prefecture, home to Chubu Centrair International Airport, announced its decision to become the first municipality in the three prefectures of the Tokai region to introduce the tax.

In Kitakyushu City, Fukuoka Prefecture, which began implementing the accommodation tax in 2020, concerns were raised by local lodging facilities prior to its introduction, with some questioning whether the tax would lead to a decline in tourist numbers. However, with an estimated tax revenue of approximately 400 million yen, the city has utilized these funds to enhance the appeal of tourism and improve the reception environment.Initiatives included further highlighting Kitakyushu’s nightscape—which was selected as one of Japan’s “New Three Great Night Views”—and installing information boards in four languages. As a result, these efforts have led to an increase in the number of tourists. In Nagasaki City, which began implementing the tax last year, tax revenue of approximately 370 million yen is projected. The city plans to allocate 60% of this revenue to the Destination Management Organization (DMO) to implement measures aimed at strengthening data analysis and improving services for visitors.The addition of the lodging tax to existing tourism revenue sources has increased funding by hundreds of millions of yen. This has enabled efforts to improve reception infrastructure, strengthen information dissemination, and reinforce the organizational structure of tourism promotion bodies such as tourism associations, thereby enhancing the competitiveness of tourist destinations.

While the introduction of the lodging tax ultimately requires approval from the Minister of Internal Affairs and Communications, the first step is to ensure that lodging businesses—who will serve as the special collectors of the tax—understand the significance and structure of the system. Following this, careful explanations must be provided to residents, and the lodging tax system must be designed with the region’s specific circumstances in mind before the ordinance can be passed and enacted by the local assembly.While it is desirable for all local residents and businesses to understand and support the measure, reaching a consensus within the community can be difficult in practice. However, there is a possibility that a significant gap will emerge in the future between tourist destinations that have secured funding through the introduction of a lodging tax and those that have not.

[Table 1] Status of Accommodation Tax Implementation Nationwide

4. Case Study: Fukuoka City

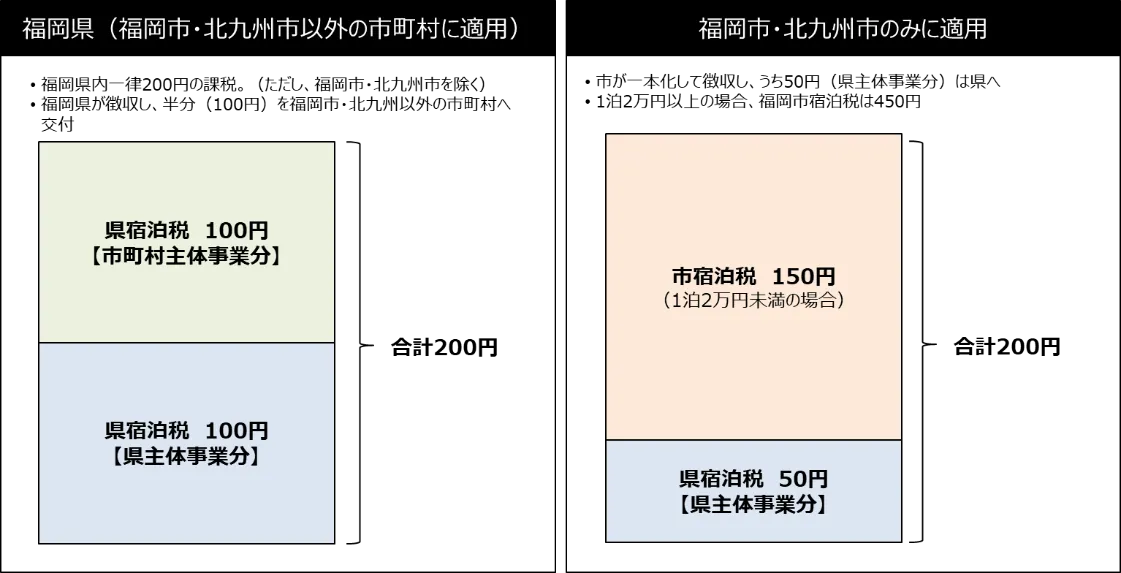

As a member of the Fukuoka City Accommodation Tax Investigation and Review Committee, which began implementing the accommodation tax in 2020, I was involved in the design of the system. At the time, Fukuoka Prefecture was also considering its introduction, and since there was no precedent for both the prefecture and the city to introduce the tax simultaneously, coordination between Fukuoka Prefecture and Fukuoka City was difficult. However, the result was an advanced system that has since served as a model.For guests staying at hotels or private lodging within the city, a tax of 200 yen (including 50 yen in prefectural tax) is levied on stays costing 20,000 yen or less,and 500 yen (including 50 yen in prefectural tax) for stays of 20,000 yen or more. In Kitakyushu City, which introduced the tax simultaneously with Fukuoka City, a flat rate of 200 yen (including 50 yen in prefectural tax) was set. In other municipalities where the accommodation tax has not been introduced, Fukuoka Prefecture collects a flat rate of 200 yen, but the revenue is split equally between prefecture-led and municipality-led projects.Recently, prefectures and municipalities have begun simultaneously considering the introduction of accommodation taxes, but I believe we should design a system that avoids double taxation for guests.

Regarding the hot spring tax in Fukuoka City, prior to its introduction, the rate was 150 yen for overnight stays and 50 yen for day trips; however, after its introduction, the rate was set at 50 yen regardless of whether the visit was an overnight stay or a day trip. Amid nationwide discussions, there are voices suggesting that the hot spring tax could be abolished after the introduction of the lodging tax. However, since managing hot springs involves separate expenses, we believe the hot spring tax should be retained, even if the amount is reduced.

[Figure 2] Accommodation Tax in Fukuoka Prefecture, Fukuoka City, and Kitakyushu City (for stays costing 20,000 yen or less)

When introducing the accommodation tax, the understanding of accommodation providers within the city is extremely important. In Fukuoka City, as part of the specific deliberations on the system, a survey was conducted among accommodation providers to investigate their concerns.The survey results revealed that a significant number of operators were concerned that the introduction of the lodging tax might negatively impact metrics such as the number of guests. Therefore, during explanatory sessions for lodging operators, the city carefully explained the significance of the tax and the benefits for accommodation facilities—such as how the revenue would be used to attract inbound tourists and strengthen MICE promotion, leading to an expansion of overall lodging demand, increased demand on weekdays, and a more even distribution of demand throughout the year—thereby gaining the operators’ understanding.

In the case of Fukuoka City, the Fukuoka City Tourism Promotion Ordinance—which stipulates the tourism measures to be undertaken by the city and the imposition of a lodging tax as a funding source—was passed by the City Council, followed by the city’s subsequent design of the system. The fact that the ordinance was passed by a super-partisan majority in the City Council was due in part to the careful explanations provided to council members and the holding of study sessions.The City Council came to understand that utilizing the lodging tax to improve infrastructure would benefit local residents, and that enhancing Fukuoka City’s international competitiveness would also be significant for the entire Kyushu region. Furthermore, efforts to gain broad public understanding were strengthened, including a special feature on the lodging tax in the “Fukuoka City Government Newsletter”—distributed to every household in the city—and communications through local media aimed at promoting understanding of the purpose of introducing the tax.

[Figure 3] Fukuoka City Newsletter “Accommodation Tax Special Feature”

Since accommodation facilities play a crucial role in increasing local tax revenue, it is necessary to provide various support measures for accommodation operators, who are designated as special taxpayers. Accommodation operators collect the accommodation tax from guests and then report and pay it to the municipality; in return for handling these administrative procedures, they receive an accommodation tax compensation payment.In the case of Fukuoka City, this incentive is set at 2.5% of the reported and paid accommodation tax amount; however, from the year of its introduction (2020) through 2024, the rate is set at a maximum of 3.5% (with a cap of 2 million yen per facility). Going forward, it will be necessary to consider measures aimed at resolving challenges faced by accommodation facilities, such as improving operational efficiency through digital transformation (DX) and providing recruitment support to address the recent issue of labor shortages.

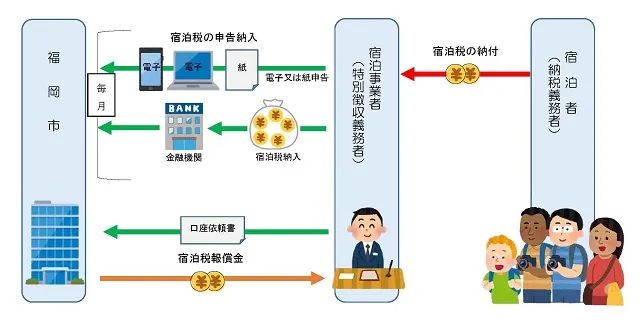

[Figure 4] Accommodation Tax Procedure Flow (Fukuoka City)

Furthermore, the most critical task following the introduction of the tax is to widely publicize how the accommodation tax is being utilized and to ensure that not only accommodation operators but also residents continuously understand the necessity of the tax. Municipalities that have introduced an accommodation tax, not limited to Fukuoka City, are disseminating information on its usage through various methods.In Fukuoka City, three years after the tax’s introduction, the “Committee for Reviewing the Implementation Status of the Fukuoka City Tourism Promotion Ordinance” was established—with the author serving as chair—to verify the implementation status of projects funded by the accommodation tax. Additionally, a survey was conducted among accommodation operators to grasp the actual conditions of accommodation facilities following the tax’s introduction and to foster understanding of various initiatives.

With a rapid increase in foreign tourists from Asian countries such as South Korea, and the successive hosting of various events including international conferences and major international sporting events like the World Aquatics Championships, Fukuoka City’s lodging tax revenue for FY 2022 reached 1.9 billion yen. Given that even medium-sized cities can expect tax revenues of 300 to 400 million yen, it is clear that the introduction of a lodging tax serves as a driving force for dramatically advancing tourism promotion.

[Figure 5] Report on Projects Utilizing the Lodging Tax (Fukuoka City)

5. Directions for Resolving Challenges Related to the Introduction of a Lodging Tax

There are four main challenges associated with the introduction of a lodging tax.

The first is the difficulty in reaching consensus among accommodation providers. Many providers are concerned about the introduction of the lodging tax, and as a result, discussions often stall.There is a persistent concern that introducing the lodging tax will lead to higher room rates and cause travelers to avoid the area; however, based on actual data following implementation, there has been no decrease in the number of guests due to the tax. For standard online reservations, the lodging tax is typically paid at check-in and is not displayed as an added amount at the time of booking. In the case of dynamic packages, the tax is included in the total travel cost, so it is collected by the travel agency.

The second point concerns transparency regarding the accommodation tax. We often hear concerns about whether the tax is being used effectively. Transparency is essential regarding the use of these funds. We must constantly demonstrate the cost-effectiveness of measures funded by these resources—for example, by strengthening tourism promotion organizations as Destination Management Organizations (DMOs), conducting data analysis, implementing effective marketing strategies, and working to balance annual demand.

The third point concerns the scope of guests subject to the tax. There is also the question of whether to collect the accommodation tax from budget accommodations costing a few thousand yen, local residents, and educational travel groups. This will be left to the discretion of each region. Establishing tax-exempt categories or exemptions could ultimately increase the administrative burden on accommodation providers. Regarding attracting educational travel groups, it may be worth considering separate incentives, or other measures such as providing subsidies when local residents use local accommodations and promote the region’s appeal via social media.

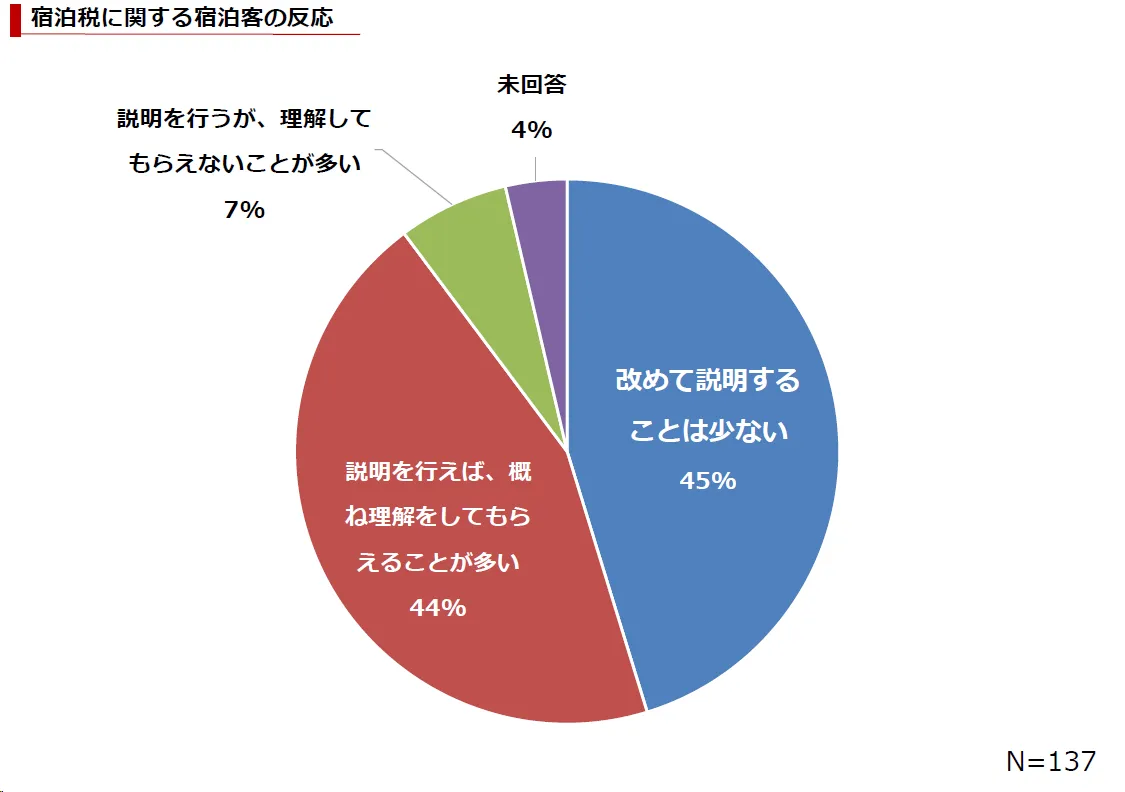

The fourth point is raising awareness and understanding of the lodging tax. Local governments must thoroughly inform visitors about the tax. Many lodging operators have expressed concerns that “visitors may not understand the need for the tax, and as a result, the burden will fall on the accommodation providers.” However, a survey conducted by Fukuoka City three years after the tax’s introduction found that regarding guests’ reactions to the lodging tax,89% of respondents reported that they “rarely need to explain it again” or that “when explained, guests generally understand.” While 7% reported that “they explain it but guests often do not understand,” we need to carefully investigate the actual situation and resolve the challenges faced by accommodation providers.

As discussed earlier, while the promotion of Japan as a tourism-oriented nation has entered a new phase in the post-COVID era, given the reality that many local governments cannot increase their tourism promotion budgets, the introduction of a lodging tax is indispensable. Although there are many hurdles to its implementation, we are now being asked whether we can overcome them for the sake of the next generation’s future.

[Figure 6] Guest Reactions to the Lodging Tax

著者