Innovation in the Travel Industry: A Community-Driven Perspective

As the tourism market undergoes transformation—with the number of international visitors reaching an all-time high—Japan’s travel industry has not yet fully capitalized on these growth opportunities. This article focuses on “regional travel businesses”—such as destination management companies (DMCs), tour operators, and land operators—that operate on a regional basis. By analyzing changes in the industry’s structure, it explores the potential for innovation that can simultaneously address regional challenges and create value.

1. Background

The year 2026 has begun. In 2025, the number of international visitors to Japan exceeded 40 million, setting a new record, and Japanese society is facing a situation unlike anything it has ever experienced before. As of November 2025, the cumulative number of Japanese travelers abroad stood at 13.44 million, a 13.6% increase from the previous year. Looking globally, while geopolitical tensions persist in some regions, travel demand remains robust. According to the World Tourism Organization (UNWTO) World Tourism Indicators, international tourist arrivals from January to September 2025 exceeded 1.1 billion, an increase of approximately 50 million compared to the same period in 2024.

Under these circumstances, if we focus on the potential for creating new demand and value, the travel business appears to retain strong growth potential going forward. In fact, within inbound travel to Japan, sectors such as adventure travel and high-value-added travel are growing as new areas, supported by national tourism policies. Unfortunately, however, it is difficult to say that the Japanese travel industry is fully capitalizing on these market opportunities. According to statistics from the Japan Tourism Agency, the total transaction volume of major travel agencies in FY 2024 was approximately 81% of the level seen in FY 2019, and as of October 2025, it had increased by 5% year-on-year. Looking solely at the transaction volume for inbound travel, it has grown to 115% of the previous year’s level as of October 2025; however, this pales in comparison to the 117.7% year-on-year growth in the number of international visitors to Japan during the same period. Furthermore, inbound travel accounts for only 6.3% of the total transaction volume of Japanese travel agencies, meaning that, fundamentally, the inbound travel business has little impact on their operations. The share of the travel distribution market held by the planning and sales of package tours—primarily for overseas travel, which has historically been the source of travel agencies’ profits—may be gradually being eroded by non-traditional business models such as LCCs, OTAs, and vacation rentals. However, market opportunities are available equally to all players. What the travel industry needs now is innovation to provide new value to new markets.

A new wind is already blowing. In June 2025, “tabinaka summit 2025” was held in Minato Ward, Tokyo, as Japan’s first tourism industry event dedicated to “tabinaka” (in-trip experiences). Despite being the inaugural event and a paid event, attendance exceeded 900 people, combining both in-person and online participants. There was a large turnout of younger generations, including volunteers. I also rushed to the venue to cheer on the organizers, and the event was filled with an energy and excitement rivaling that of “Arival,” a series of events focused on in-trip experiences held around the world. This year’s event is scheduled for Friday, June 12. As the market reaches a turning point, I would like to consider how the travel industry can view this as an opportunity for innovation to transform itself and chart a course for delivering new value.

2. Structural Changes in the Travel Industry—2017–2018 as a Turning Point

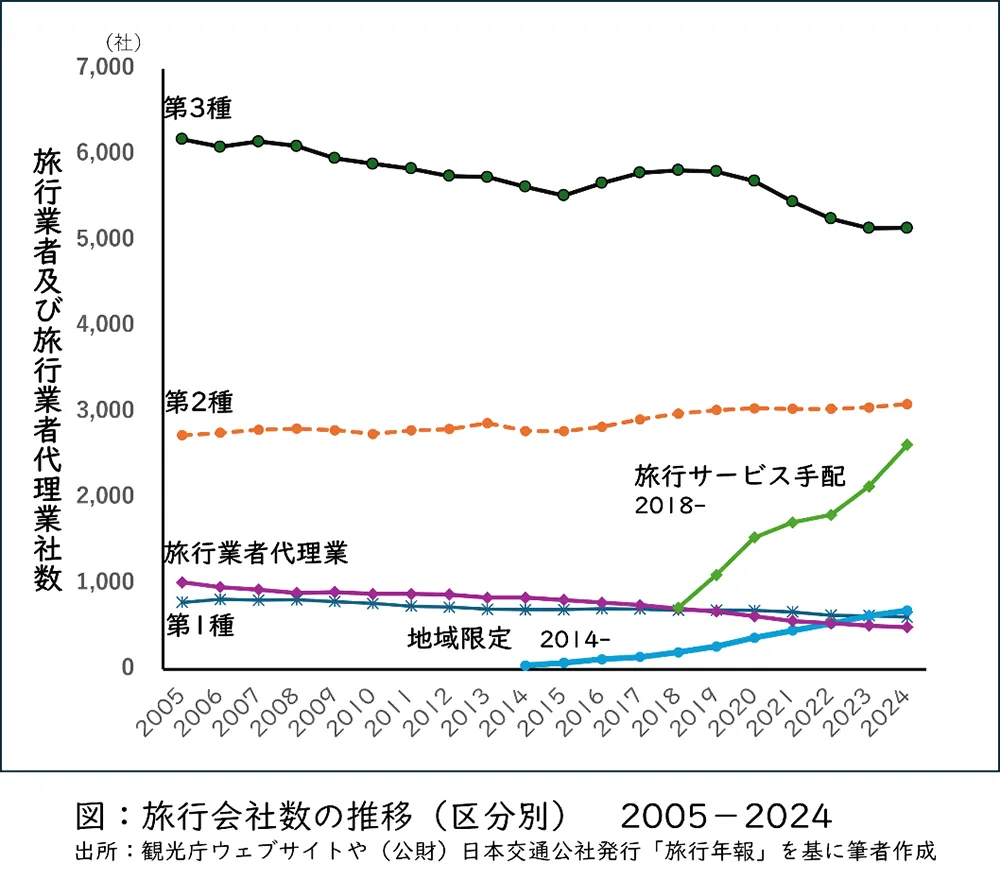

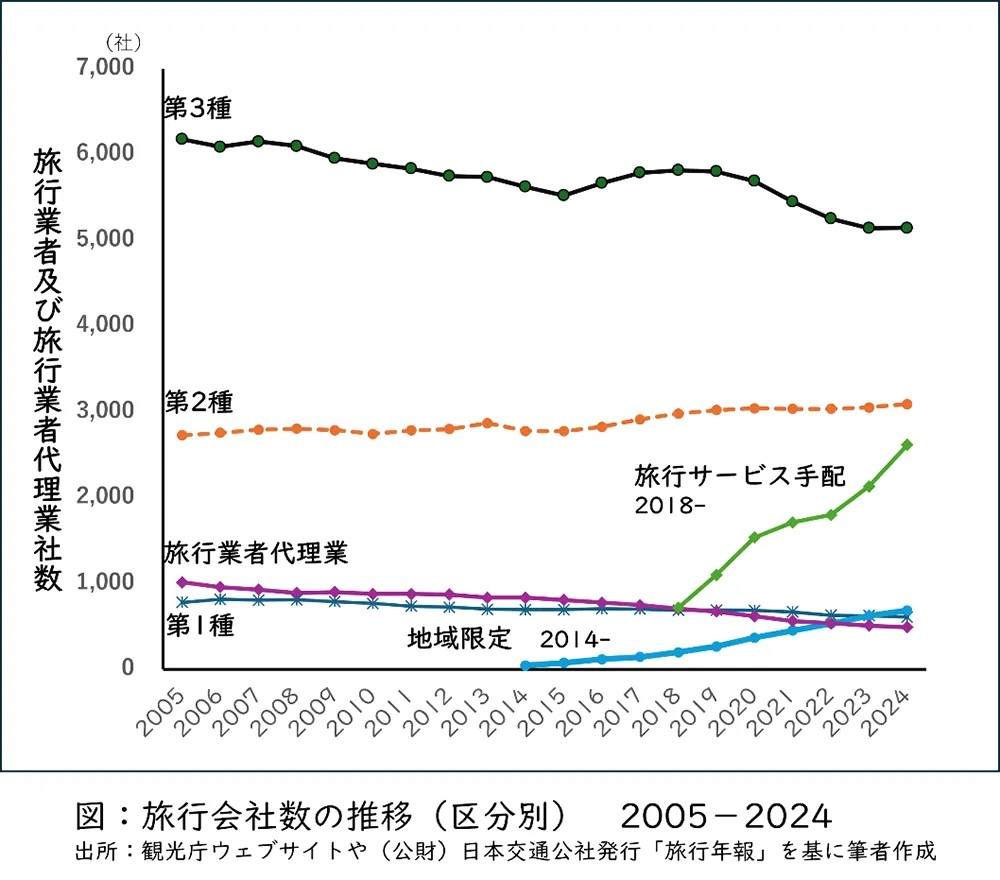

In Japan, the travel business is classified according to the scope of services it can handle under the Travel Agency Act. It is broadly divided into three categories: travel agencies, travel agency agents, and travel service arrangers. Travel agencies are further subdivided into four categories: Type 1, Type 2, Type 3, and regionally limited.

An analysis of the trend in the number of registered travel agencies from 2005 to 2024 (Figure) shows that the number of Type 1 travel agencies—which can handle both domestic and international travel and include major companies such as JTB and HIS—stood at 781 in 2005, 20 years ago, but will drop to 609 in 2024, a decrease of 172 companies, or approximately 20%.The number of registered Type 2 travel agencies, which handle only domestic travel, remained below 3,000 from 2005 to 2014, but exceeded 3,000 in 2019 and reached 3,091 in 2024, representing a 13% increase. Type 3 travel agencies and travel agencies decreased by 83.3% and 48.5%, respectively.

The regionally limited travel agency category, established in 2013, restricts the scope of travel products it can handle to departure points, destinations, and accommodations located within the municipality where the business office is situated or in adjacent municipalities. The number of registered companies in this category has increased steadily since the system’s introduction, reaching 687 in 2024.A detailed analysis of the growth pattern over the 11 years since the system’s introduction reveals that the growth trend was not uniform; rather, with the period around 2017–2018 serving as a turning point, the growth rate has been higher than before. In other words, this suggests that a structural change occurred in the Japanese travel industry during this period (Note 1).

3. Regional Travel Businesses Handling Local Departure and Arrival Travel Products and Destination-Based Tourism

One factor behind this structural shift is the DMO (Destination Management Organization) registration system, introduced in 2015 as part of a strategy to revitalize regions through tourism. Organizations that meet the registration requirements set by the Japan Tourism Agency are registered as “Registered DMOs.” As of October 2025, there are 334 Registered DMOs and 29 Candidate DMOs (the Candidate DMO system was abolished at the end of September 2025, but existing Candidate DMOs may continue to operate until their renewal deadline at the end of September 2028).DMO stands for Destination Management/Marketing Organization. Distinct from traditional tourism associations, DMOs aim to establish organizations that promote effective destination marketing and sustainable regional development while strengthening the local economy; as part of these activities, they are promoting travel that originates and terminates within the region. Although the data is somewhat outdated, survey results indicate that approximately 90% of DMOs handle locally sourced travel products as a means of securing independent revenue (Akiyama, Suzuki, 2021).

Amid these trends, travel businesses based in tourist destinations—such as DMCs (Destination Management Companies), land operators, and tour operators—are attracting attention. While these business models have long been known in the travel industry, they are increasingly recognized as key players as policies promote the sophistication of destination management and initiatives targeting new markets, such as high-value-added travel and adventure travel. The author collectively refers to these as “regional travel businesses” and will briefly introduce each business type below.

First, regarding DMCs, according to ADMEI, the U.S.-based trade association for DMCs, they are defined as “specialized service companies based in travel destinations that leverage local expertise and resources; as strategic partners, they provide creative local experiences in event management, tours/activities, transportation, entertainment, and logistics. ”Believed to have originated in Europe and the U.S. in the 1970s, many companies today have expanded their services beyond MICE to leverage their expertise in highly specialized travel arrangements, such as SIT (Small Group Tours) and adventure travel.

Next, land operators primarily handle various travel arrangements at tourist destinations upon request from travel agencies in the departure region. Overseas, they are often referred to as tour operators or ground handlers. In Japan, following the 2018 amendment to the Travel Agency Act, registration with the prefectural governor as a “travel service arrangement business” became mandatory.

The third category, tour operators, differs from the previous two in that they primarily take the initiative in planning their own travel products. While similar to Japanese “travel agencies,” they are often based in tourist destinations and are therefore sometimes called “incoming (inbound) tour operators.” Although they aim to sell their independently planned travel products directly to consumers, they often partner with other travel agencies as part of their distribution strategy.

However, these distinctions are not strictly applied in the business world, and the terms are sometimes used interchangeably. For example, while the Adventure Travel Trade Association (ATTA) lists “Tour Operator” as a category in its membership directory but not “DMC,” many companies that call themselves DMCs are found within the “Tour Operator” category.

Meanwhile, in Japan, “destination-based tourism” and “destination-based travel” (Note 2) have been promoted in various regions since the 2000s. This refers to regions taking the lead in planning and operating travel products; while it is a concept similar to the regional travel business, it is likely more common in terms of tourism policy.

However, it is often understood that planning and developing these locally-based tours does not generate profit. There are two possible reasons for this. First, destination-based travel has been implemented with local governments and tourism associations taking the lead and utilizing public funds such as subsidies. It was also often planned and executed only on specific dates or for limited periods as “monitor tours. ”While the programs themselves focused on unearthing the local culture and history—aspects that had previously been overlooked—and involved stakeholders from primary industries, offering experiences difficult to achieve through standard travel products, they were not expected to generate sufficient profits to benefit the local economy. The second reason is the deep-rooted perception among major travel agencies that “destination-based travel and local departure travel products are not profitable. ”This is because, unlike the business model that generates profits through so-called “transportation-inclusive” products—which, like overseas package tours or group tours, include transportation to the destination—these products have traditionally been priced at lower rates. Previously, a manager in charge of planning local-departure optional tours in Europe told me: “Most employees at major travel agencies have only experience planning tours that depart from the origin city; few understand the know-how of the local-departure tour business, so it’s very difficult to explain to them.” This suggests that the local-departure travel business requires a different business strategy than traditional models.

Given the reality that local-departure travel businesses are operating worldwide, this does not mean that destination-based travel is inherently unprofitable; rather, it suggests that it has not been implemented as a profitable business model. In other words, if local-departure travel is recognized as a distinct business format and a new business model—and if the know-how for implementing it is widely shared—it has the potential to revolutionize the existing travel industry, create new players, and revitalize the market. In that sense, there remains ample room for innovation in the travel business.

4. The Two Values of Regional Travel Businesses

Local travel businesses will likely become indispensable in the future as the missing piece in promoting tourism that coexists with the local community. This is because, due to their characteristic of conducting business rooted in the local community, local travel businesses play two important roles. First, they play a role in delivering unique local travel products to the market through distribution (distribution co-creation role).Second, they play a role in building networks and promoting collaboration not only with local tourism operators but also with local residents serving as guides, as well as those in agriculture, forestry, and fisheries—stakeholders essential to advancing tourism today (the role of regional co-creation).

For example, “Oki Tabikousha,” based on Okinoshima Island in Shimane Prefecture, acts as an incoming tour operator, planning and selling travel products that depart from and return to the Oki Islands (Okinoshima, Nishinoshima, Nakanoshima, and Chiburijima).The “Bull-Pushing Walk Experience Tour,” said to be based on a local tradition dating back to the era of Emperor Go-Toba, involves walking with a bull used in the traditional bull-pushing ritual while chatting with the herder. Although the tour consists solely of walking with the bull, it is well-received by participants. However, it is not easy to help herders—who are not tourism professionals—understand the know-how and significance of hosting tourists, making the establishment of local relationships essential for bringing such initiatives to fruition.

The two roles of the local travel business are interrelated and reinforce each other, forming a sustainable system—an ecosystem. In other words, while it is difficult for local operators to manage alone, distributing travel products—including via the internet—allows them to grasp market trends and consumer needs. By feeding this knowledge back into the community, they strengthen trust with local stakeholders. Furthermore, new ideas born from understanding the latest customer needs lead to the creation of new product value, enabling the provision of fresh offerings to distribution channels. Such a sustainable system differs significantly from one-off, subsidy-driven destination tourism initiatives. The regional travel business can act as a catalyst for building a sustainable ecosystem within the region while simultaneously generating profits as a business entity in its own right.

5. Conclusion: The Potential of Regional Tourism Businesses to Address Local Challenges

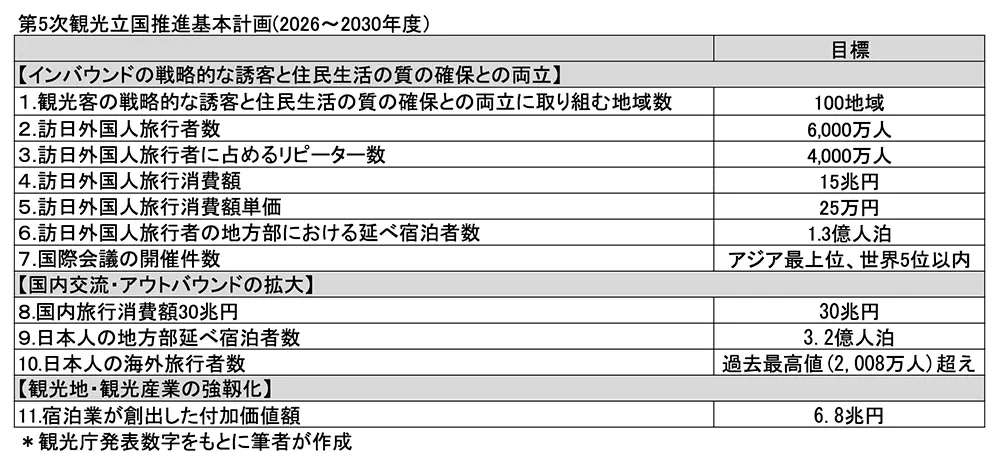

The Fifth Basic Plan for Promoting Japan as a Tourism Nation will commence this April. Discussions to date within the Tourism Subcommittee of the Ministry of Land, Infrastructure, Transport and Tourism’s Transport Policy Council have identified one of the desired outcomes as not merely increasing tourist numbers, but rather improving satisfaction for both local residents and tourists. Consequently, managing tourist destinations will increasingly require striking a balance between tourism and the quality of life for residents. Due to the proliferation of social media and excessive “content tourism,” the temporary concentration of tourists in specific areas—leading to overcrowding—is often cited as “overtourism,” which negatively impacts residents’ daily lives. On the other hand, Japan boasts abundant natural and cultural resources across the country, and there is a growing need for tourism that utilizes these resources in a sustainable manner to bring economic and social benefits to local communities. We aim to effectively leverage the role of local travel businesses, such as DMCs and tour operators, as key players in achieving this. Specifically, to avoid the concentration of inbound tourists in popular tourist destinations and encourage them to visit a wider range of regional areas, it is important to implement policies that foster DMCs and tour operators as key players responsible for arranging travel within the region.

In promoting regional tourism policies, the local travel industry serves as a valuable collaborative partner for DMOs. DMOs are public-sector organizations that market and manage regions, and their activities often lead to business opportunities. As business partners to whom overseas travel agencies specifically request quotes and arrangements, this role—being a commercial activity—is not inherently part of the DMO’s public duties but rather falls under the purview of the local travel industry. Overseas destinations maintain lists of locally based DMCs, and some even have industry associations. However, there is a widespread consensus that Japan currently faces a severe shortage of DMCs. In fact, this shortage is hindering efforts to capture new markets, such as adventure travel. The report from the Adventure Travel World Summit Hokkaido, Japan (ATWS2023), held in September 2023, also recommends fostering DMCs, which play a central role in developing adventure travel products. While the importance of guides in adventure travel goes without saying, the presence of business entities responsible for distribution and product delivery is indispensable. Furthermore, it is crucial that a shared understanding spreads among general consumers that a new type of travel business—distinct from traditional travel—is necessary.

For local communities, realizing tourism that contributes to regional development will become increasingly important in the future. In the past, the travel industry “invented” travel products and played a part in realizing mass tourism—an era where anyone could travel easily and affordably—thereby driving social transformation. Today, as we are called upon to address numerous social challenges such as a declining birthrate and an aging population, as well as regional revitalization, we aim to redefine our value proposition by viewing these solutions as business opportunities. We are committed to working closely with local communities to contribute to their development, and we aspire to demonstrate our value as a game-changer that realizes tourism capable of solving regional challenges.

Note

- (1) In a breakpoint analysis covering the period from 2014 to 2024, 2017 was identified as the most significant turning point, with the largest difference in regression slopes before and after that year at 49.70. The second-largest difference (46.39) occurred in 2018 (Kobayashi, 2025).

- (2) While “destination-based travel” and “destination-based tourism” have strictly different meanings, they are treated as synonymous in this paper. For details, refer to “Regional Travel Business Theory” (by Hirokazu Kobayashi).

References

- Kobayashi, H. (2025) Transformation of the tourism system and the rise of destination-based travel businesses — An exploratory analysis based on travel industry data in Japan (2015–2024), 74th AIEST ABSTRACT BOOK, p.19

- Akiyama, Y., & Suzuki, S. (2021) A Study on the Planning and Operation of Destination-Based Tourism by Japanese DMOs: Based on a Questionnaire Survey on Destination-Based Tourism Conducted by the Japan Tourism Agency Among Registered and Candidate DMOs. Proceedings of the 36th Annual Conference of the Japan Society for Tourism Studies (December 2021), pp. 77–82

- Japan Tourism Agency, Ministry of Land, Infrastructure, Transport and Tourism (2024) Results of Hearings and Surveys Aimed at Promoting Adventure Tourism in Light of ATWS2023

- Hirokazu Kobayashi (2022) Regional Travel Business Theory, Koyo Shobo

- Inbound Web Magazine Yamagokoro.jp

著者