[Special Feature] “Tourism x LCC”: What Is “LCC 2.0,” the Concept Shaping the Future of Aviation?

Although LCCs are often described as cheap but cramped, some passengers have noted that the seats don’t actually feel that cramped. As they align with a value system that prioritizes cost-effectiveness, they have become widely established. This can be considered the “LCC 1.0” phase.Recently, airlines have been required to demonstrate a sustainable approach to aviation, such as reducing CO2 emissions. Therefore, in this article, using the keyword “LCC 2.0,” we will propose a vision for next-generation aviation that contributes to society.

1. The Rising Popularity of LCCs, Driven by a Trend Toward Selective Spending

Low-cost carriers (LCCs) began operating in Japan in 2012, attracting so much attention that the term was even selected as a buzzword of the year. Jetstar Japan, a major LCC, has promoted the benefits of “smart, savvy spending”—offering low fares and allowing travelers to use the money they save for other purposes—under the slogan “Smart and Savvy. ”A survey by JTB Tourism Research & Consulting (*1) also found that “low cost” was the top reason for using LCCs. It is true that initially, there were negative perceptions, such as the seats being cramped despite the low fares, airports being far away and inconvenient, and usage rules not found with existing full-service carriers (hereinafter referred to as FSCs). Despite these perceptions, LCCs have become firmly established thanks to growing customer understanding.

As of 2021, the revenue per kilometer for LCCs stands at 5.9 yen, which is approximately 40% of the 15.1 yen recorded by FSCs. Furthermore, their market share has expanded to 16% of all domestic air passenger traffic in Japan (*2).

However, is “low cost” their only strength and appeal?

2. Airline ESG Strategies Centered on Market Changes

In the post-COVID environment, attitudes toward work styles have also begun to shift. Remote work has lowered the barriers to living in remote areas, and lifestyles that involve commuting between major cities and regional areas have gained attention. Furthermore, from the perspective of revitalizing regional economies, there are many examples of airlines—led by FSCs—collaborating with local governments to promote dual-residence living. However, aren’t LCCs, which can easily establish themselves as everyday lifestyle infrastructure by leveraging low fares, the most suitable candidates to serve this role?

In the aviation industry, business demand is declining due to changes in work styles driven by the widespread adoption of web conferencing. We anticipate that the leisure and VFR (visits to friends and relatives) markets will recover first, while business demand will remain sluggish for the long term. For example, according to ANA’s mid-term management strategy for 2018–2022, announced before the COVID-19 pandemic, the company planned to reduce domestic FSC passenger volume to 97% of 2017 levels by 2022. Conversely, for its LCC operations, ANA announced plans to double passenger volume by 2022 compared to the same period, citing steady growth in passenger demand. This plan remains in effect even amid the pandemic.

The downward trend in fares is likely to continue, along with the resulting pressure to cut costs. Furthermore, airlines must adapt to the revitalization of local economies through increased tourism revenue, environmental considerations through CO2 emission reductions, and the diverse lifestyles spreading throughout society. While responding to the demands of these diverse stakeholders and addressing corporate management challenges, the expansion of the LCC business is becoming increasingly important. The key point here is to rebrand LCCs as an “environmentally friendly mode of transportation” that goes beyond mere cost-effectiveness, and to position them as the “very heart of ESG management” for the company.

3. The High CO₂ Emissions of FSCs: A Potential “Achilles’ Heel”

Recently, efforts to realize a sustainable society have been gaining momentum. The aviation industry is no exception. The high-density seating arrangement in LCCs has achieved low fuel consumption per seat at the cost of cramped conditions. This also translates to reduced CO₂ emissions.

With that in mind, I conducted a fuel efficiency comparison.

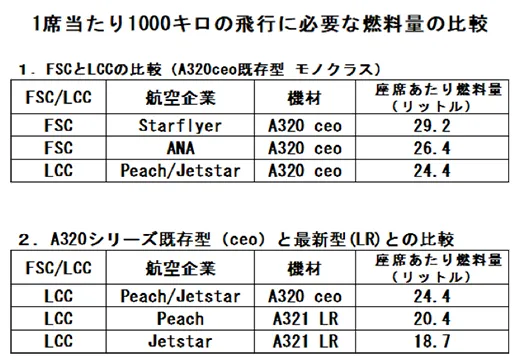

Even with the same aircraft model, differences in route characteristics, seat count, and class configurations between airlines result in variations in aircraft weight and fuel consumption. Furthermore, figures released by aircraft manufacturers often have different underlying assumptions, leading to discrepancies with the data reported by airlines. Therefore, I first calculated the fuel consumption required for a single aircraft to fly one kilometer based on the fuel tank capacity and range published by the manufacturer. I then divided this by the actual number of seats operated by each airline to determine and compare the fuel consumption per seat. The following shows the fuel consumption per seat required for an Airbus A320 series aircraft to fly 1,000 kilometers.

(1) Comparison of FSCs and LCCs (A320ceo (existing model), single-class)

Here, we will compare the A320ceo (conventional model).

FSCs prioritize comfort and therefore feature a more spacious seat configuration. ANA, an FSC, configured 166 seats on this model (*3). In this case, 26.4 liters were required. StarFlyer, another FSC, operates aircraft with an even more spacious 150-seat configuration. This requires 29.2 liters. On the other hand, LCCs such as Jetstar Japan and Peach Aviation configure their aircraft with 180 seats, resulting in a fuel consumption of 24.4 liters. Compared to StarFlyer, these LCCs consume 17% less fuel.

(2) Comparison of the Existing Model (ceo) and Latest Model (LR) of the A320 Series Operated by LCCs

Let’s examine the differences between the existing model (ceo) and the latest model (LR) of this aircraft series as operated by LCCs.

As mentioned earlier, both Peach Aviation and Jetstar Japan recorded a fuel consumption of 24.4 liters per 100 km with the existing model (ceo).Both airlines have now begun operating the latest model, the A321LR. However, there is a significant difference in seating capacity between the two. Peach Aviation, with 218 seats, recorded a fuel consumption of 20.4 liters—4 liters less than the existing model. Jetstar Japan, on the other hand, has 238 seats and achieved an even lower consumption of 18.4 liters. The reasons for the difference in seat count between the two airlines are: (1) Jetstar’s aircraft are specifically configured for domestic and short-haul international routes; and (2) Peach, on the other hand, needs to operate medium-haul international flights that take advantage of the aircraft’s long range. To ensure sufficient fuel capacity for long-haul flights within the specified maximum takeoff weight, Peach had no choice but to set its payload capacity (in this case, the number of seats) lower. Additionally, (3) by reducing the number of seats, Peach was able to increase seat pitch, which led to improved comfort, particularly on long-haul flights.

Currently, Jetstar Japan’s A321LR has the lowest CO2 emissions per seat, with figures 36% lower than those of StarFlyer, a full-service carrier (FSC).

Here, I would like to touch on the initiatives aimed at achieving carbon neutrality by 2050, which form the core of the ESG management pursued by each company.

JAL has announced three pillars: “1. Upgrading to fuel-efficient aircraft (contribution to CO2 reduction: 50%),” “2. Operational improvements (contribution to CO2 reduction: 5%),” and “3. Utilization of SAF (Sustainable Aviation Fuel, an alternative to fossil fuels) (contribution to CO2 reduction: 45%)” (*4).Regarding "1.," which accounts for the largest share of the reduction, it is important to note that the company has only mentioned "upgrading to fuel-efficient aircraft for the time being" and has not provided more meaningful data, such as figures broken down by FSC and LCC.As mentioned earlier, the market share of LCCs, which have lower CO2 emissions, is expanding. Although the company plans to expand its LCC operations, specific information regarding revenue and profits from this segment has not been disclosed. FSCs, which generate more than double the revenue per passenger compared to LCCs, remain a critical revenue source. Given that FSCs still account for a significant portion of the company’s revenue, we believe it will be difficult for the expansion of the LCC business to offset the contraction of the FSC business in the near term.

Airlines are carefully avoiding making statements regarding these weaknesses of FSCs. In other words, could the high CO2 emissions of FSCs be described as their “Achilles’ heel”?

4. Toward the Era of “LCC 2.0”

For airlines to achieve sustainable growth, they must look to the future and offer new value to passengers and society. If the current focus on cost-effectiveness and targeted spending represents “LCC 1.0,” I would like to propose “LCC 2.0” as a model that goes beyond it.

This means that LCCs go beyond mere cost-effectiveness to become an environmentally conscious “smart choice.” By anticipating the future to achieve net-zero—a state where CO2 and other greenhouse gas emissions in 2050 balance out with the amount removed by humans—this represents a path toward evolving from “selective consumption” to “ethical consumption.”

As mentioned earlier, such initiatives could have unintended consequences for airline management. However, to accelerate the realization of the carbon-neutral goal by 2050—a pillar of our mid-term management plan’s ESG strategy—we must leverage the strengths unique to LCCs and drive this initiative forward.

In a lecture, economist Yusuke Narita offered the following perspective on how to drive social change: “If there are people who can overcome the challenges of our time, they are not those who simply build upon past successes. To do so, it is necessary to recognize that ‘we may actually be harming society.’”

For airlines to earn a higher level of social trust, they must make efforts to disclose information regarding CO2 emissions, distinguishing between full-service carriers (FSCs) and low-cost carriers (LCCs).

Furthermore, they must explore a new model for aviation that lies beyond the extension of past experiences. In a sense, this may only be achievable through the deconstruction and subsequent reconstruction of the FSC business model. It will be a grueling process that transcends conventional wisdom and sometimes requires deliberately embracing difficulties. “LCC 2.0” will likely materialize only in exchange for such blood, sweat, and tears.

Beyond this “creative destruction,” the future of aviation will be revealed, and I cannot help but feel that LCCs will be the main players in this new era.

Footnotes:

(※1) JTB Tourism Research & Consulting, “Survey on LCC Users’ Attitudes and Behavior 2017,” August 4, 2017

(※2) Author’s calculations based on data from the Ministry of Land, Infrastructure, Transport and Tourism, “Disclosure of Information on Air Services (Specified Air Carriers)”

(※3) Although this domestic-spec aircraft has now been retired, it is used here for comparison purposes

(※4) JAL, “JAL Group Mid-Term Management Plan for FY2021–2025”

著者